How Specialised Loans for Auction Investments Work

Auctions are high-stakes events where timing and liquidity mean everything. The rare painting, gemstone, or collectible often appears once, and buyers must be ready to act fast. But many investors, collectors, and firms do not keep millions of dollars sitting idle in their accounts. This is where specialised auction loans step in. Unlike standard credit lines, these loans are designed to match the pace and nature of bidding. They give participants the ability to move quickly, secure lots, and pay later under structured terms. Understanding how these loans work helps explain how modern auctions function and why more people rely on financing to compete in this world.

The Rise of Auction Financing

In the past, auctions were the domain of wealthy individuals or institutions with large reserves of cash. That has changed dramatically. Today, banks, private lenders, and specialised financial firms provide short-term loans tailored to auction dynamics. The logic is simple: assets purchased at auctions often carry stable or even appreciating value, making them suitable collateral. This allows lenders to extend credit quickly and with less risk. For participants, it means they do not have to liquidate existing portfolios or tie up capital in anticipation of bidding. Auction financing has opened the field to a broader base of collectors, investors, and even companies, turning auctions into increasingly competitive financial ecosystems rather than gatherings of a cash-rich elite.

Why Timing Is Crucial

Unlike other markets, auctions operate on strict schedules. If you are not ready to pay, you cannot participate. Specialised loans align with this need for immediate access, with approvals often happening in days or even hours. The speed is part of what distinguishes auction financing from traditional loans.

How Specialised Auction Loans Work in Practice

The structure of an auction loan is designed to mirror the rhythm of bidding and settlement. A borrower approaches a lender before the auction with details about the type of lot they intend to pursue. The lender then assesses the applicant’s financial standing and, in many cases, the estimated value of the asset being targeted. Once approved, the loan is ready to be drawn immediately after the hammer falls. Repayment terms vary but are usually short—often months rather than years—since the expectation is that assets may be resold, refinanced, or integrated into an existing collection. Interest rates are higher than standard loans due to the speed and risk involved, but the convenience and access often outweigh the cost for bidders.

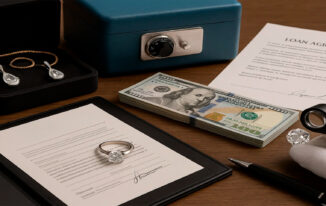

Collateral and Security

The lot itself frequently serves as collateral. Once the item is secured, it may remain in escrow or under joint control until repayment is complete. This reduces risk for the lender while allowing the buyer to finalize the acquisition. Some lenders also require additional collateral or guarantees, particularly for high-value or volatile assets.

Risks for Borrowers and Lenders

As with any credit product, specialised auction loans come with risks. Borrowers face the obvious danger of overbidding, encouraged by the availability of financing. A winning bid that exceeds market value can leave them with debt and an overvalued asset. Liquidity risk is also real: if repayment depends on quickly reselling the asset, market conditions must cooperate. For lenders, the risks lie in valuation errors, market downturns, or disputes over authenticity. Because auctions often involve unique items, determining accurate collateral value is challenging. To mitigate these risks, lenders lean heavily on expert appraisers, legal checks, and insurance coverage before funds are released.

The Psychology of Borrowing at Auctions

Financing does more than provide money—it changes behavior. Bidders with loan support may feel empowered to go higher than they would with cash alone. While this can lead to acquisitions that build value, it can also inflate prices or lead to regrets if the market cools. The psychology of borrowed money is a central element of why auction loans must be used carefully.

Different Models of Auction Financing

Not all auction loans look the same. Some are structured as bridge loans, meant only to cover the gap between purchase and longer-term financing. Others are revolving credit facilities tailored for frequent bidders who participate in multiple auctions each year. Private lenders often offer bespoke deals with flexible repayment structures, while banks may tie loans to broader wealth management products. The diversity reflects the wide range of participants in modern auctions, from individual collectors to corporations and investment funds. Each model has advantages and trade-offs, and successful borrowers are those who align loan structure with their specific auction strategy.

Bridge Loans for Auctions

Bridge loans are among the most common solutions, providing immediate liquidity for acquisitions that will later be refinanced. They are short, intense bursts of financing, often repaid within months.

Revolving Credit for Frequent Collectors

For active participants who attend multiple auctions annually, revolving credit allows continuous access to funds without renegotiating new terms for each event. This model resembles business credit lines but is tied to high-value assets.

The Global Context of Auction Loans

International auctions in cities like New York, Geneva, and Hong Kong attract participants from around the world. This global scope means auction financing often involves cross-border lending, foreign currency exposure, and varying legal frameworks. Lenders with international expertise play a key role in making these loans practical. They help borrowers navigate exchange risks, import/export compliance, and differences in property law. For borrowers, choosing a lender with global reach can make the difference between a seamless acquisition and a complex legal struggle. As auctions expand into digital platforms, global financing strategies will become even more critical, allowing borrowers to secure assets regardless of location.

Cross-Border Challenges

Borrowers face unique hurdles when bidding overseas: fluctuating exchange rates, customs clearance, and differing legal recognition of collateral. Lenders that specialize in international auction finance provide tools such as currency hedging or escrow arrangements to smooth these challenges.

Forward-Looking Perspectives

The world of auction financing is evolving alongside the broader financial industry. Digital platforms now allow remote participation in major auctions, which is likely to increase demand for fast, digital-first loan products. Blockchain-based authentication and escrow services may streamline collateral verification, reducing lender risk and speeding up approvals. Ethical and sustainability considerations are also creeping into the conversation, especially in markets for gemstones, antiquities, and cultural heritage items. Banks and financial firms may soon condition loans on stronger compliance with sourcing standards. In the long term, auction loans may become fully integrated into wealth management, with investors treating auctions not as occasional events but as part of broader portfolio strategies. The tools will become more sophisticated, but the principle remains the same: providing liquidity at the exact moment it is needed.

Technology’s Role in the Next Phase

Artificial intelligence and digital analytics may soon allow lenders to make faster, more accurate decisions on asset value and borrower risk. This could lower costs and expand access, bringing auction finance to a wider base of participants.

Conclusion

Specialised loans for auction investments represent the intersection of finance and passion. They allow bidders to act decisively in competitive markets without tying up all their capital. While the risks are real—ranging from overbidding to market volatility—the careful use of auction loans can unlock opportunities that would otherwise remain out of reach. For lenders, these products provide exposure to unique asset classes backed by tangible collateral. For borrowers, they are a gateway into a fast-moving, high-value world where timing is everything. As auctions become more global and more digital, financing solutions will continue to adapt, offering sharper, faster, and more secure ways to participate. In the end, auction loans are not just about money—they are about access, strategy, and the ability to seize opportunities that appear once and may never return.